If you’re having a hard time saving money, you’re not alone.

In fact, you’re in the majority as 69% of Americans have less than $1,000 in their savings. This isn’t a majority you want to be part of!

Thankfully, there are so many great apps out there that can help build your savings almost on autopilot, one of them being the Digit app. While it won’t make you a millionaire, it can easily surpass that $1,000 balance most Americans don’t have.

In this review, I wanted to talk about the Digit app and how it can help you save almost on autopilot. Near the end, as with all of my reviews, I will give my take as to whether or not it’s worth it.

Digit Saving App Review

What is Digit?

Digit is a popular financial company that analyzes your spending and will automatically save the perfect amount so that you don’t have to think about it. I will get into how the app works later in this review, I promise.

In 2017, Fast Company named it as one of the most innovative finance companies, and it continues to grow to this day, securely saving more than one billion dollars! It’s 100% legitimate and you can be assured that your money will be in good hands. Your data is secured by 256-bit encryption and all of your money will be held at FDIC insured banks.

Instead of focusing on your future retirement, the app moreso focuses on saving a few dollars here and there to save for your future or maybe something else you have in mind. Whether you want to use this money for an emergency fund, your child’s college education or a vacation, it’s up to you as to how you want to spend it. It’s a great app idea if you have a hard time saving money and need that discipline to do so.

In the end, the app was designed to be as stress-free as possible when saving your cash for anything you have in mind.

Signing Up

To sign up with Digit, they will first ask that you give them your phone number and create a password. As this app works a lot with text messages, it’s extremely important that you sign up with a phone you readily have available and one that accepts text messages. As you use the app, it will report to you to show you how much you have been saving. This can be helpful to let you know when you’re close to reaching your goal.

Also, since the app needs to transfer money from your savings/checking account and help you save, you will also have to link one of your bank accounts. I know this can be scary for some, but all transfers are encrypted and your credentials will never be accessible to the app as they use Plaid to link your accounts. You can be assured that your bank account is in good hands. Just remember that if you don’t link a savings/checking account, you won’t be able to use the app.

To link your account, it’s very easy. You will just click on your bank logo, sign in to your account via the app and enter your banking credentials. Again, the app does not see this information. As I write this, Digit works with more than 2,500+ banks.

Right now, only U.S. residents can sign up.

Getting Started

After you connect your bank account and sign up, the app will now analyze your activity, basically looking as to how much money comes into your account as well as how much your remove through spending, etc. This can take a few days or weeks before it’s able to figure how much it should start taking out.

Once its algorithm has a feel as to how much you spend, it will then start to save for you, effectively taking a certain amount of money and transferring it to your Digit savings account. Again, these savings accounts operated by Digit are FDIC insured, simply meaning that your first $250,000 is covered by the U.S. government.

The amount Digit takes will greatly depend on your spending habits as mentioned and what the app thinks you can afford to save.

So, for example, if you have $1,500 in your account and have close to $1,200 in bills due based on your past history, then Digit may only take out a few dollars, but if you have more than $1,000 with no upcoming bills projected in the next 30 days, then it may take out much more.

Regardless of what your account looks like, Digit will never take out more than $150, but you can control these aspects via your settings if you’re uncomfortable with this amount. You can also stop Digit if need be.

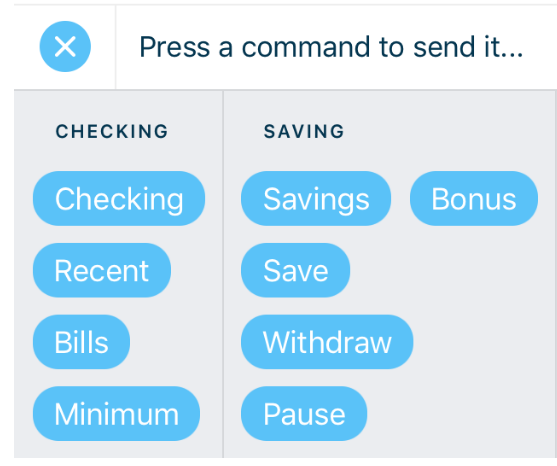

Texting

Since Digit is set up like a bot, you will have to communicate with it via text message using specific commands, most of which seen here after signing up…

“Recent,” for instance, tells you the most recent transactions, whereas “Save” will move that much money to your digit account.

After you sign up, the app will walk you through the process, but just let it be known that you will have to text to get what you want. The commands are pretty straight-forward, but it’s best to know everything you can do as the bot can understand quite a bit.

Setting Goals

Once you set up your app, you can set up what’s known as “saving goals,” and you can create as many as you want. In creating these goals, you can create your own or choose one of the predefined options. Just add a description, set an emoji for reference, the amount you’d like to save, and when you’d like to save it by. Then, as you use the app, you can text Digit with that emoji to see how you’re doing or even add a “boost” if you want to save more than you usually do.

You can set as many goals as you want. There is no limit.

In the end, everyone’s results will be different, but just let it be known that it will help you save money and meet your goals eventually.

What happens if they take too much?

A common concern from what I researched was what if Digit took too much money out of your account, effectively leaving you with a negative balance?

Since almost all banks will charge you with an overdraft charge, it would definitely be unfair to you if you had to pay it when you had money in the first place.

Well, thanks to Digit’s overdraft assurance, they will reimburse you up to two instances of an overdraft. You can read more about their policy in detail here.

How do I withdraw money?

As your money will be transferred to a Digit savings account, you can always withdraw money at any time, 24/7, 365 days a year. It works just like a bank account, wherein you will simply log in or even text the app to let it know how much money you want back in your account.

Thre are no limits as to how often you take out money and no fees to pay.

Savings Bonuses Are Possible!

The great thing about Digit is that they will reward you with a 1% annualized savings bonus if you save with Digit for three consecutive months.

If at all possible, make sure you keep the app active for three+ months to take advantage.

Outside of the bonuses, the app does not pay out interest like most savings accounts, so this could be viewed as a negative to some.

A Thing to Note

Since Digit uses a specialized algorithm to figure out your spending habits, it’s very important that all of your money comes out of the said account. With that being said, a big downfall to most is that you have to use your debit card almost extensively if you want to capitalize on saving.

Because the app determines how much to save based on both your deposits and spending, it can really throw off the algorithm if you use a bank account/credit card outside of the account connected to the app. The same can be said if you find yourself using cash a lot.

While this can be a downfall to most, I just wanted to mention this as some people are uncomfortable solely using their debit card.

Digit FAQ

You may have other questions, so I wanted to create a quick section answering any questions you may have.

Is it free?

No. Unfortunately, if you want to use Digit, it will cost $5 per month; however, if you view it as a financial advisor, it’s not much at all! You can cancel at any time. If you’re a first-time user, you can try it free for 30 days.

Is the Digit app safe?

Absolutely. As mentioned, the company uses state-of-the-art security measures, securely storing and anonymizing any information they have about you. All funds held are FDIC insured.

Where does my money go?

Once Digit starts taking out money, you will get your own Digit savings account that will hold your savings. Much like any other savings account, you can withdraw money at any time. You will be able to access your funds via the app 24/7, 365 days a year.

Do I get bank interest?

No. You can receive bonuses as mentioned, but your money will not incur interest over time.

Pros and Cons

As with all of my reviews, it isn’t always about me, so I wanted to let you know what others thought of the app, listing both the pros and cons below. I found most of these pros and cons simply by looking at the reviews others left on the app’s official page in the Google Play Store.

The Pros

- free 30-day trial

- 4.3/5 Google Play rating

- FDIC insured

- 1% savings bonus

- overdraft protection

- easy to save without thinking

- no minimum to get started

- can make changes via text message

- very easy to use

The Cons

- $5/month to use

- no interest outside of savings bonus

- have to use your debit card for accurate results

- limited customer service

- the algorithm can be unpredictable

- not ideal for retirement savings

Final Thoughts

If you have a hard time saving money, then Digit can work for you. While they do charge a small $5 fee, I think it’s an awesome way to save money for anything if you don’t have the discipline to do so. As the app takes money out here and there, I don’t even think you will notice. Those little withdrawals really do add up!

While I wouldn’t recommend it as a way to save for your future retirement, it can make for a fantastic way to save for anything you need for the future, whether it be a vacation or even a new car. Just remember you won’t see any interest on your savings, so I wouldn’t recommend saving too much money. Kind of picture it as a way to save up for something and then spend it.

If you can save money and have the discipline, then you’re better off setting up free saving accounts with banks like Ally and creating automatic transfers on your own. That way, you can control the entire aspect and not have to pay that monthly fee. Plus, you can get paid interest.

Regardless of which option you choose, you can’t go wrong with savings. Whether it’s the app or doing it on your own, make it your goal right now or continue to do so if you’re already saving right now. Your future self will thank you!

If you have used the apps and/or have any concerns, then you’re more than welcome to leave your comments below! I will try my best to help.

Want $5 free?Try out Swagbucks, the most popular reward program I make the most money with. Simply answer survey questions and get paid! Join Now to Get $5! |

Add comment